Macroeconomic conditions

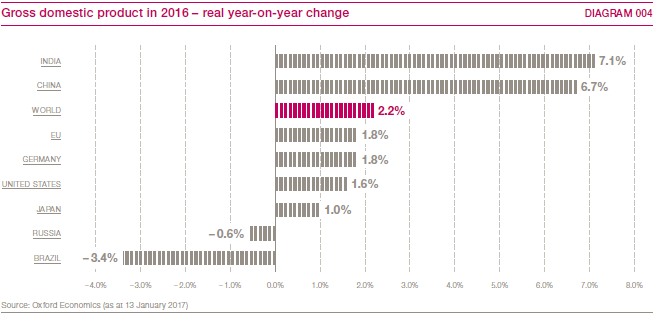

In 2016, the global economy expanded at a slower rate than in the previous year due to weaker growth in the United States, the European Union and China. Growth in global trade also persisted at a low level in 2016 and fell well short of expectations. The influencing factors were the weaker economies of the major emerging markets China and Brazil as well as declining US imports. In addition, companies also held back on capital equipment spending due to the uncertain prospects. However, consumer spending was encouraging – as it had been in 2015.

The economies of the European Union registered modest growth, albeit slightly slower than in the previous year. Nonetheless, companies viewed their situation much more optimistically again at the end of the year. The surprising outcome of the United Kingdom’s referendum on whether to leave the European Union did not have any significant impact on the eurozone in 2016. The UK economy remained fairly steady on the whole, although heightened uncertainty caused companies to scale back capital expenditure.

Following a very weak start to the year, the United States saw its growth pick up significantly in the second half of the year thanks to a positive trend in the job market and strong domestic demand. Exports were also better than expected.

In China, the growth rate slowed moderately – as had been anticipated – and the shift away from industry towards the service sector continued. Domestic consumption remained robust, partly because of the government’s economic stimulus package. Particularly in the second half of the year, the Chinese economy expanded at a faster rate again than in the previous months.

Although Russia’s growth continued to slow in 2016, it showed signs of stabilising at the end of the year. The Brazilian market’s sharp downtrend persisted despite improved sentiment among consumers and companies following a change of leadership. > DIAGRAM 004